How much do I need to save for retirement?

Table of Contents

How much do I need to save for retirement?

2 Mar 2023

How much do I need to save for retirement?

It’s the million-dollar question, isn’t it? To help you find that ‘magic number’, here are some tools, tips and insights from Kōura.

-

Focusing on your weekly retirement income instead of the lump sum

-

Figuring out how much weekly retirement income you need

-

Understanding where that weekly retirement income will come from

-

Bridging the gap in order to reach your retirement goal

-

Turning the weekly income into a lump-sum amount.

To help us visualise this, let’s introduce you to John, a 30-year-old plumber who currently earns $80,000 and is trying to figure out how much he needs to retire. So, let’s get started.

1. Focus on your weekly retirement income instead of the lump sum

Want to understand how much you need to save? It’s a good idea to think about your retirement savings in terms of weekly retirement income, rather than focusing on the lump sum.

Why? Because big numbers are difficult to grasp. If we told you that you’re on track to get $451,000 with your KiwiSaver plan, that would sound like a lot. But in weekly income terms, it would only give you $632 including NZ Super. How does that compare to your current income? And would it be enough to fund your retirement goals?

For example, John currently takes home $1,136 per week. So, a retirement income of $632 would only replace 55% of his current income. Would that be enough to meet his future needs? Let’s dig a little deeper.

2. How much weekly income will you need?

We get it – estimating your future expenses can be a complicated task. To simplify things, we recommend this three-step process:

-

Start with a basic weekly budget – Of course, you don’t know what the world will look like by the time you retire. But you can make some assumptions, based on the post-work life you want to live. Think about your current expenses minus those you will no longer have (like kids’ education, mortgage payments, car repayments etc.). Then add in the extra things you’d like to do with your newfound spare time (like travelling costs or picking up a hobby) and how much those would cost. Lastly, finish up with a 10-20% buffer for unexpected expenses. What’s the number?

-

Consider the income replacement rule: A common guideline is to save enough to replace between 70% and 100% of your current income; less (70-80%) if you will retire with a mortgage-free home, more (100%) if you will be renting for life. For example, if you earn $1,200 per week after-tax, you may need between $840 and $960 including NZ Super if you’re a homeowner, and $1,200 if you’re renting. What’s your target range?

-

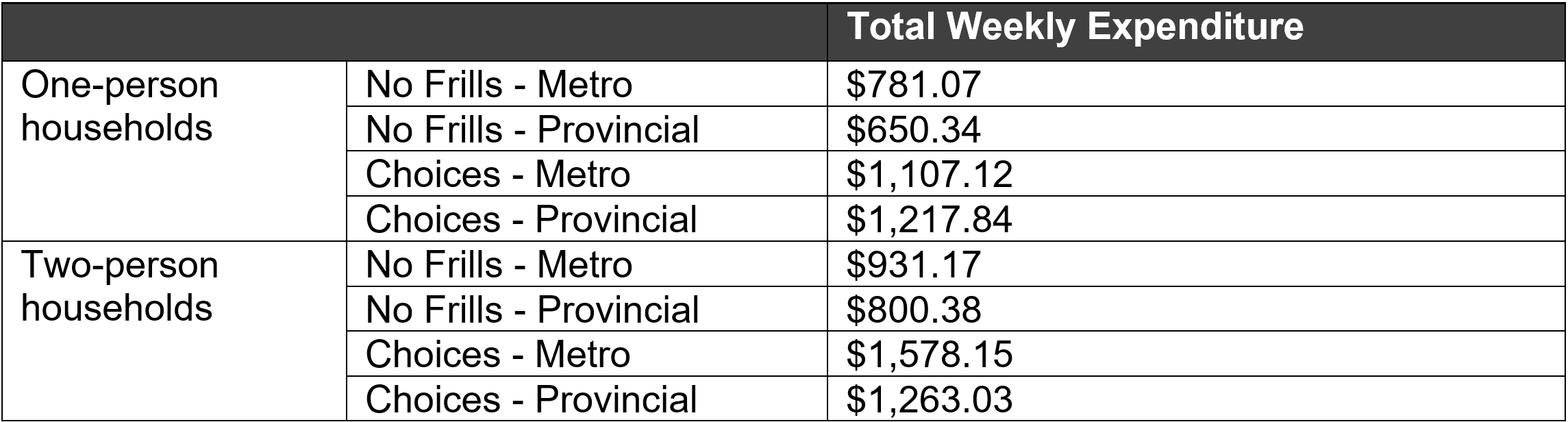

Compare this number with the NZ Retirement Expenditure Guidelines: Every year, Massey’s Fin-Ed Centre publishes a report outlining how much Kiwi retirees are currently spending in excess of NZ Super. These are just rough estimates and won’t be relevant for everyone, but it helps put your estimated weekly income into context. See the table below for reference.

Source: Massey University’s Fin-Ed Centre, Retirement Expenditure Guidelines 2022(1)

Let’s go back to John, then. He owns a home and is on track to enter retirement mortgage-free. To John, retirement means more time to do the things he enjoys, like travelling around New Zealand and overseas, but also spending quality time in Auckland with friends and family.

Applying the 70-100% rule of thumb, he would need between $795 and $900 a week (70% and 80% of his current income, respectively). But comparing this with the NZ Retirement Expenditure Guidelines, it looks like John may need a little more, so he’s considering replacing 100% of his current income of $1,136. Which brings us to the next question…

3. Where will your weekly income come from?

At the moment, most of your income comes from work earnings. Saving for retirement means putting aside enough money that you will no longer need to work to sustain your lifestyle. So, you may want to start off with what you currently expect.

Your future weekly income may come from any of the following:

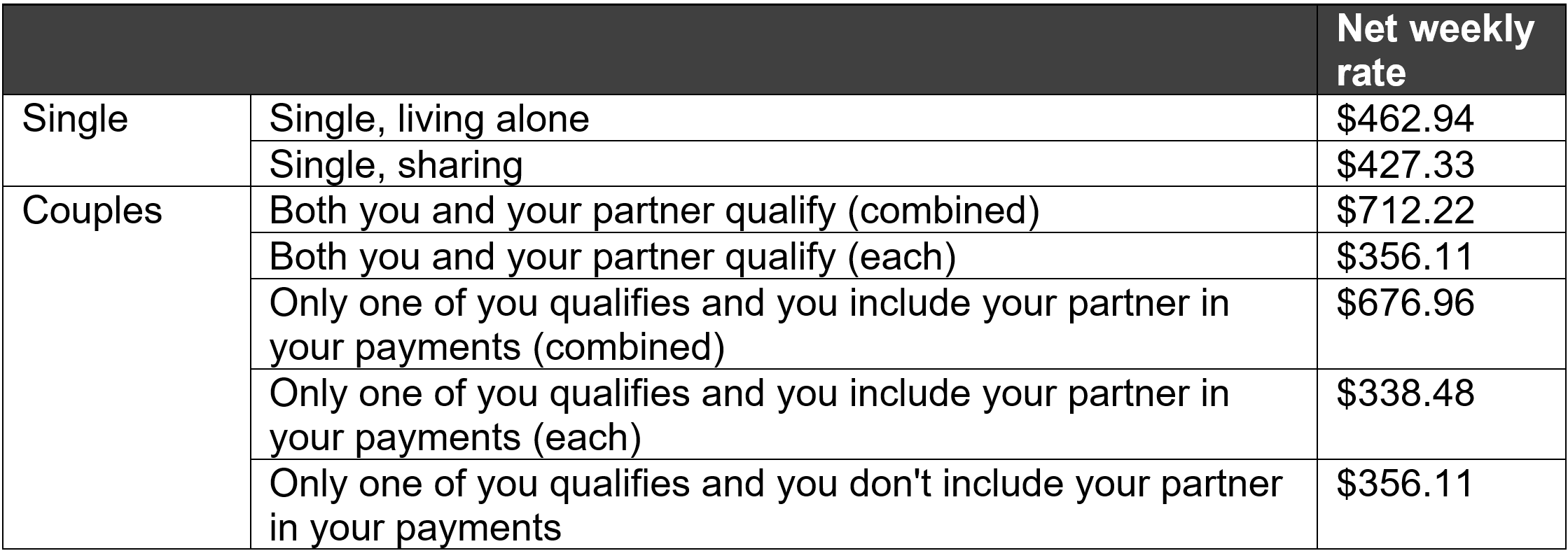

- NZ Super – New Zealand superannuation is a universal state pension that the government pays fortnightly to New Zealand residents aged 65 and over who meet the residency criteria. NZ Super rates are adjusted 1 April each year, in line with inflation. Here are the current rates at 1 April 2022.

Source: WorkandIncome.govt.nz, 2022(2)

-

Property investments that you have or plan to make – There are essentially two ways to go about property investing. You can either invest in rental properties for rental yield (which would provide a passive income in retirement), or invest for capital gains, sell the property and add the sales proceeds to your nest egg. Either way, there are potential risks and costs to consider, including property market volatility. As always, better not to put all your eggs in one basket and rely solely on one asset for all your retirement needs.

-

Other investments – A well-balanced, diversified investment portfolio can be another great tool to boost your retirement savings over time. If you’re not investing yet, it may be something worth considering.

-

KiwiSaver – And of course, you may have a KiwiSaver plan in place. But just signing up to the scheme is not enough: you also need to choose a fund that’s aligned with your risk profile and an appropriate contribution rate, then continue to review things over time. We’ll get back to it shortly.

-

Other income sources – You might also have other assets to leverage, for example you own home. Being a homeowner gives you the option to sell and downsize, freeing up the equity you’ve built.

Now, think about what you expect to receive from the income sources you have in place. Then, compare that with your expected spending. Is there a gap? And if so, how wide?

John is expecting to use his KiwiSaver plan and NZ Super. Using the current rates, NZ Super will provide him $338.5 of his retirement weekly income. To replace 100% of his current income ($1,136) in retirement, his KiwiSaver savings will need to provide him with $797.5 per week. To replace 70% ($795), their KiwiSaver savings will need to provide $456.5 per week.

4. How to bridge the gap between expected spending and income

-

Consider adding extra income sources – If your budget allows it, you can look at expanding your investment portfolio, for example by dipping your toes in property, investing in the sharemarket, or using KiwiSaver.

-

Make the most of what you have – Are you getting the most out of what you already have, including your KiwiSaver plan?

With KiwiSaver in particular, a small change like increasing your contribution rate can make a big difference down the line. Like to know how big? Our digital advice tool allows you to understand how different contribution rates may change the outcome. Just select a higher rate and see how much extra you can save.

As the graph shows, to be able to replace between 70% and 100% of his pre-retirement income, John would need to choose a KiwiSaver contribution rate of 6% and over. As we said, the 70-100% range is just a rule of thumb, but it gives you a starting point to work on and finetune into a more accurate figure.

This scenario is based on a $0 KiwiSaver balance with a starting salary of $80,000 growing at 3.5% per annum between the ages of 30 and 65 using a neutral Kōura glide path. We have used the FMA prescribed returns for our growth assumptions:

-

All equity funds are expected to generate a return after tax and fees of 5.5%;

-

Our fixed income fund is expected to generate a return after tax and fees of 2.5%;

-

Our cash fund is expected to generate a return of 1.5%.

We assume 2.0% annual inflation, the mid-point of the Reserve Bank of New Zealand’s inflation targets.

5. Turn your weekly income into a lump-sum amount

With your estimated weekly retirement income in hand, it’s time to turn that into a lump-sum KiwiSaver savings amount.

That’s your end goal, in dollar figures, and this is a simple formula to get it: you need to multiply your weekly income by 52 (the number of weeks in a year), and then multiply that for the number of years you’d like your savings to last.

-

Multiply $1,100 by 52 = $57,200 (your annual retirement income);

-

Multiply $57,200 by 30 (years) = $1,710,000 (the lump-sum amount you’ll need at retirement from all available income sources).

Are you on track? It’s time to run your numbers

-

The projected value at 65.

-

Your forecast weekly income at retirement, including and excluding NZ Super.

-

The percentage of current income you’d be able to replace with KiwiSaver.

-

The recommended portfolio for your risk profile, needs and goals.

You can also adjust the mix of variables (like your contribution rate or desired retirement age), to determine the impact on your savings. It’s a wealth of information and it takes just a few minutes to get it.

References

-

Massey University’s Fin-Ed Centre, Retirement Expenditure Guidelines 2022, September 2022

-

Work and Income, Benefit Rates, April 2022

Disclaimer: Please note that the content provided in this article is intended as an overview and as general information only. While care is taken to ensure accuracy and reliability, the information provided is subject to continuous change and may not reflect current developments or address your situation. Before making any decisions based on the information provided in this article, please use your discretion and seek independent guidance.