October market update

October market update

5 Nov 2021

October – Getting back off the mat

After a punishing September (global markets fell 3.6%), October saw a recovery, and new records reached, delivering a global market return of 5.5%.

Every time we think markets are on the ropes and starting to get wobbly legs a new bout of optimism occurs. October’s optimism was driven by extremely strong corporate earnings, increasing signs that the summer Covid resurgence is under control in the US, and continuing economic recovery in the US and Europe.

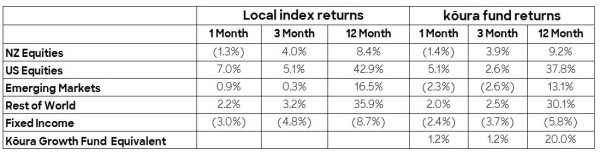

[1] Kōura Growth Fund based on a typical 80:20 mix, NZ Equities 20%, US Equities 35.4% Emerging Markets 8.4%, Rest of World Equities 16.2%, Fixed Income 20%

The New Zealand dollar is one of the best indicators of risk - it rallies strongly when investors want to take on more risk and suffers when investors are nervous about the global environment. The NZD rallied back up to almost 0.72c against the USD from a low of 0.69c in September. This strengthening of the NZ dollar has unfortunately impacted returns in New Zealand dollars.

Corporate earnings continue to shine

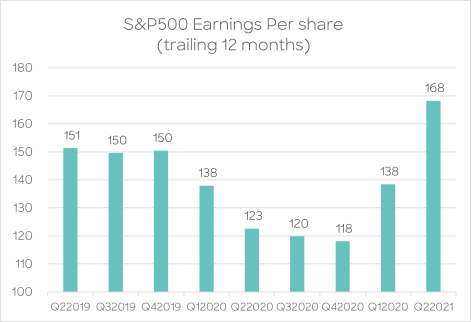

Corporate earnings continue to be materially ahead of already high estimates. As you can see from the chart below, earnings have absolutely taken off over the past 12 months and are already 12% higher than pre-covid estimates. Despite the Covid induced summer slowdown and weaker than expected economic data, Corporates continue to deliver extremely strong results ahead of expectations. During the month of October, 80% of companies reported earnings higher than expected and operating margins came in at a massive 13% vs an estimate of 8%.

Companies are adapting extremely well to the new supply chain constraints and continue to benefit from the cashed up consumer. If anything, the current set of results demonstrates the strength of corporate America at the moment and their ability to impose ongoing price rises on consumers.

Mixed economic data

Economic data continues to be mixed.

In the USA Jobless claims remain persistently high and fewer jobs are being created than economists had forecast or expected. Though consumer confidence remains high and GDP growth, whilst slowing has not slowed as much as potentially feared. A big positive was that quarterly wage growth of 5% YOY was the strongest it has been for over 20 years. Economists are confident that the worst of the pandemic is over, and the dampened economic activity seen over the summer as a result of the surging virus is now behind us. Consumer confidence was significantly higher than forecast.

We are seeing the opposite in China where consumer spending is slowing as a result of ongoing lockdowns and uncertainty around the property sector. GDP growth has slowed, and the sacrosanct 6% growth target might be at risk for 2021. Consumer spending and GDP data have both disappointed and come in below expectations.

European data on the other hand remains broadly in line with expectations with growth and consumer confidence inline. The issue though is that consumer confidence remains very muted, you still have a population worn down by a difficult pandemic, rising case numbers in a number of countries and a history of 15 years of underperformance, so it will take time for consumers to return to confidence.

Transitory inflation vs inflation caused by transitory factors

Economists have recently changed their tone, whilst acknowledging that the inflation is no longer transitory, they now argue it is caused by transitory issues (supply chain disruptions and spending Covid lockdown savings). In our view, this is semantics and probably the start of a long journey to acknowledging that we are seeing higher inflation than expected. Strong wage growth driven by a shortage of workers will drive ongoing and permanent inflation even when the supply challenges disappear.

The rapidly growing inflation numbers have resulted in central banks around the world continuing to reassure markets that interest rate rises are a long way away.

Bond markets continue to support equity markets

Despite the high levels of inflation and clarity from the US Federal Reserve around removing economic support, bond markets are still pricing in a low growth, low inflation environment. Bond yields have strengthened with the US 10-year treasury sitting at 1.55%, though this is significantly lower than the highs of 1.8% reached earlier in the year and definitely does not allow any room for significant interest rate rises to fight persistently high inflation.

As we have discussed many times, lower bond yields make the case for equities stronger as it is harder to earn a return with any other alternative investments. In particular, lower bond yields support higher valuations for the high growth technology industry where earnings are not forecast to plateau for another 5 or 10 years.

The NZ market continues to go move sideways

The NZ market was slightly down in the month falling by 1.4%. Over the past 2 years it has not seen the rally enjoyed by many other markets. As we have talked about in the past this is due to the market structure; a high exposure to a small number of companies (Fisher & Paykel Healthcare and previously A2 Milk), very few high growth tech companies, and a high exposure to the infrastructure sector. At this stage in the cycle and with the structure of the NZ market, it is hard to see that changing. Though these characteristics should mean that the NZ market holds up well if we do see another market downturn.